Blog > Appraisal vs. Home Inspection: What Buyers Need to Know Before Closing

Appraisal vs. Home Inspection: Why They’re Not the Same Thing

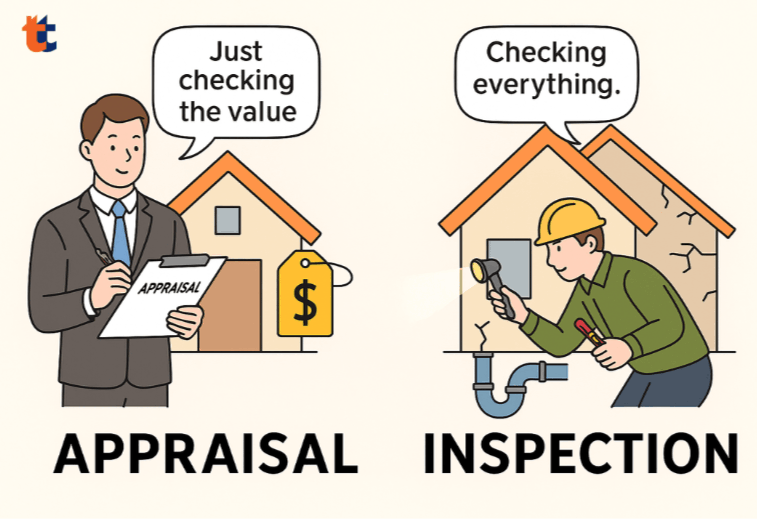

If you're buying a home, you’ve likely heard the terms appraisal and home inspection tossed around — and maybe even interchangeably. But they serve very different purposes, and confusing the two could lead to some costly surprises.

The Appraisal: For the Lender, Not You

The Appraisal: For the Lender, Not You

An appraisal is required by your lender to determine the market value of the home. It’s how the bank decides how much they’re willing to lend. The appraiser evaluates:

-

Recent sales of comparable homes

-

The home’s size, location, and condition (from a value standpoint)

-

General market trends

But here’s the catch: The appraisal isn’t looking for problems like a leaky roof, faulty wiring, or mold in the basement. That’s where the home inspection comes in.

But here’s the catch: The appraisal isn’t looking for problems like a leaky roof, faulty wiring, or mold in the basement. That’s where the home inspection comes in.

The Home Inspection: For YOUR Protection

The Home Inspection: For YOUR Protection

A home inspection is optional — but highly recommended. The inspector works for you, not the bank, and gives a full assessment of the home’s condition.

They’ll check:

-

Plumbing, electric, HVAC systems

-

Roof, foundation, attic, and insulation

-

Signs of damage, deterioration, or safety issues

Bottom line: The inspection helps you make an informed decision and potentially negotiate repairs or price reductions.

What About Termite and Water Tests?

What About Termite and Water Tests?

Some loan programs (like VA or PFHA in PA) do require additional inspections:

-

VA Loans: Often require a termite inspection and a water test if the home is on a private well.

-

PFHA: A Pennsylvania program that helps with down payments and closing costs. It also typically requires a termite inspection.

But these are loan-specific requirements — not full home inspections.

Don’t Skip the Inspection

Don’t Skip the Inspection

Even if your lender doesn't require it, skipping the home inspection is like buying a used car without popping the hood. Sure, the paint might look good — but what’s underneath?