Blog > The Myth of 20% Down — Why You Don’t Need to Wait to Buy a Home

The Myth of 20% Down — Why You Don’t Need to Wait to Buy a Home

"I was just asked this question again, so let’s clear something up..."

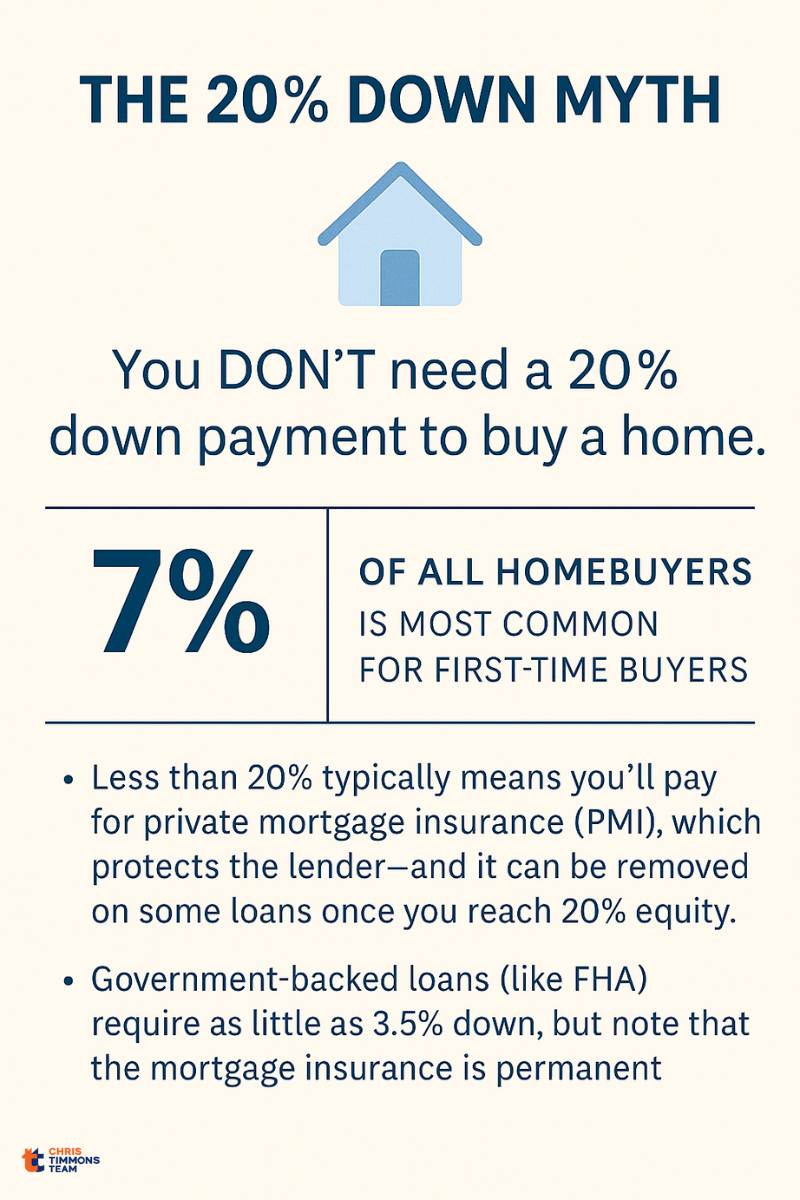

One of the biggest myths in real estate is that you have to put 20% down to buy a home. It’s a misconception that stops so many would-be homeowners from even exploring their options — and it’s simply not true.

Let’s break it down:

You Can Buy With as Little as 3% Down

You Can Buy With as Little as 3% Down

Yes, seriously. Depending on your situation and loan type, you might only need:

-

3% down on some conventional loans

-

3.5% down for an FHA loan

-

0% down for VA or USDA loans, if you qualify

Many of these programs are available to first-time buyers, buyers with moderate incomes, or those purchasing in eligible areas.

So Where Did the 20% Number Come From?

So Where Did the 20% Number Come From?

20% down is just the amount that allows you to avoid private mortgage insurance (PMI). It’s not a requirement.

In fact, putting 20% down is often not the best financial decision — especially if it drains your savings or delays your ability to start building equity.

What About PMI (Private Mortgage Insurance)?

What About PMI (Private Mortgage Insurance)?

Yes, if you put down less than 20%, you’ll likely pay PMI — but here’s what most people don’t realize:

-

PMI isn’t forever. With conventional loans, you can request PMI removal once you’ve built up 20% equity — either through payments or appreciation.

-

You can “pay it away.” Some conventional loans offer options where you pay a slightly higher interest rate or a one-time fee at closing to eliminate PMI altogether.

-

FHA is different. FHA loans come with mortgage insurance that typically doesn’t go away — it stays for the life of the loan unless you refinance into a conventional loan later.

-

PMI isn’t always expensive. For many buyers, the monthly PMI cost is surprisingly affordable — and far less than the cost of continuing to rent.

Waiting Could Cost You More Than PMI

Waiting Could Cost You More Than PMI

Here’s the kicker: home prices and interest rates don’t wait.

Let’s say home prices go up 5–10% while you’re waiting to save that elusive 20%. Not only is the home you wanted now more expensive, but your monthly payment probably is too.

The Bottom Line

The Bottom Line

You don’t need 20% down.

You need a plan, a solid lender, and a real estate agent who will help you explore all your options. Don’t let outdated advice or internet myths hold you back from taking the first step toward homeownership.

If you’re curious what options are available to you right now, shoot me a message. You might be closer than you think.